|

Mortgage Rates had Little Impact on Home Prices in July

We’re officially in our country’s longest economic expansion. The National Bureau of Economic Research reports that as of July 2019, we broke the 120-month record of economic growth experienced from March 1991 to March 2001.

In May, the unemployment rate dropped to 3.6%, which is the lowest we’ve seen since 1969. Consumer spending is up a point from last year, and retail sales are up over the last few months.

Despite this economic growth, the Federal Reserve (the Fed) lowered the Federal Funds Rate by a quarter point on July 31st, signaling that the economy needs a bit of a push.

Why?

First, despite this record-setting run, Gross Domestic Product (GDP) only grew cumulatively by 25%, which is far slower than previous expansions. Furthermore, the Consumer Price Index (CPI), which is a measure of overall inflation, sits stubbornly below the Fed’s target of 2%.

The Fed seems to be wrestling with the reality of slowing growth, an aging workforce, and low inflation across the United States. In fact, they labeled the rate decrease a ‘readjustment’ to get interest rate policies in-line with this new economic paradigm.

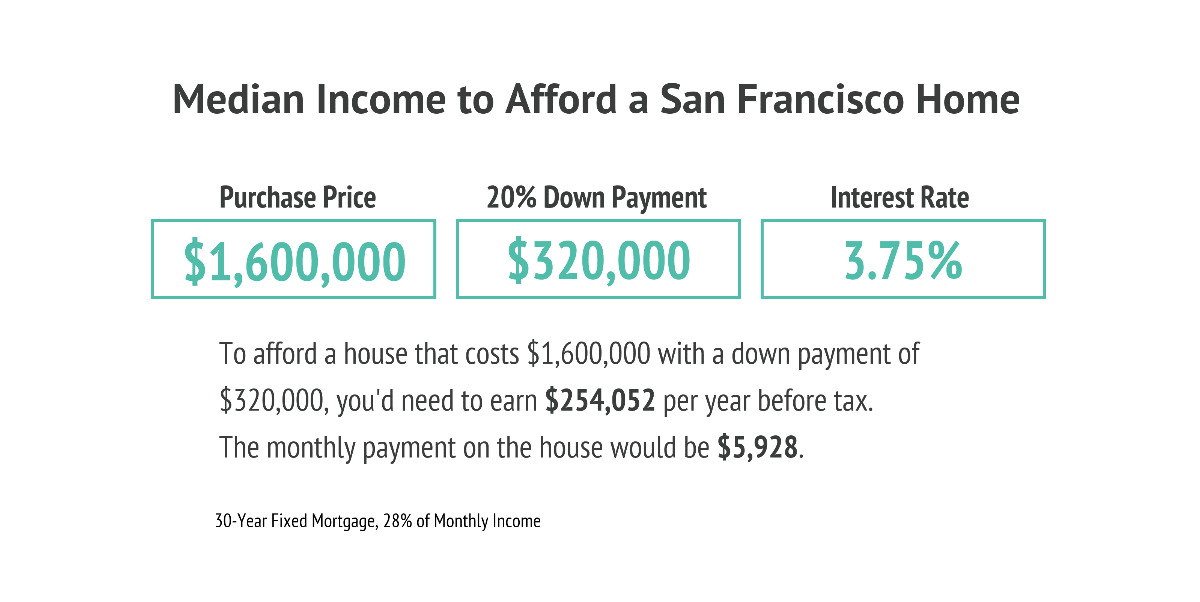

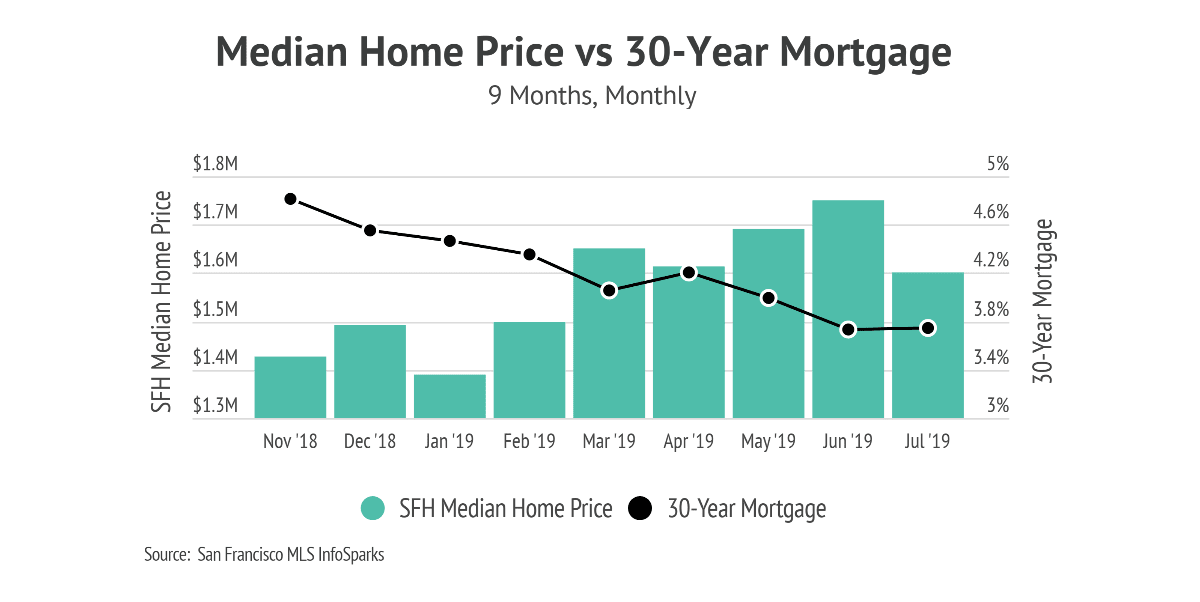

The Federal Funds Rate indirectly affects consumer borrowing costs, including mortgage rates. For example, Freddie Mac reports that the 30-year-fixed mortgage rate, which fell to 3.75% last week, is down by more than one percentage point since 2018.

This illustrates that for now, low interest rates are here to stay.

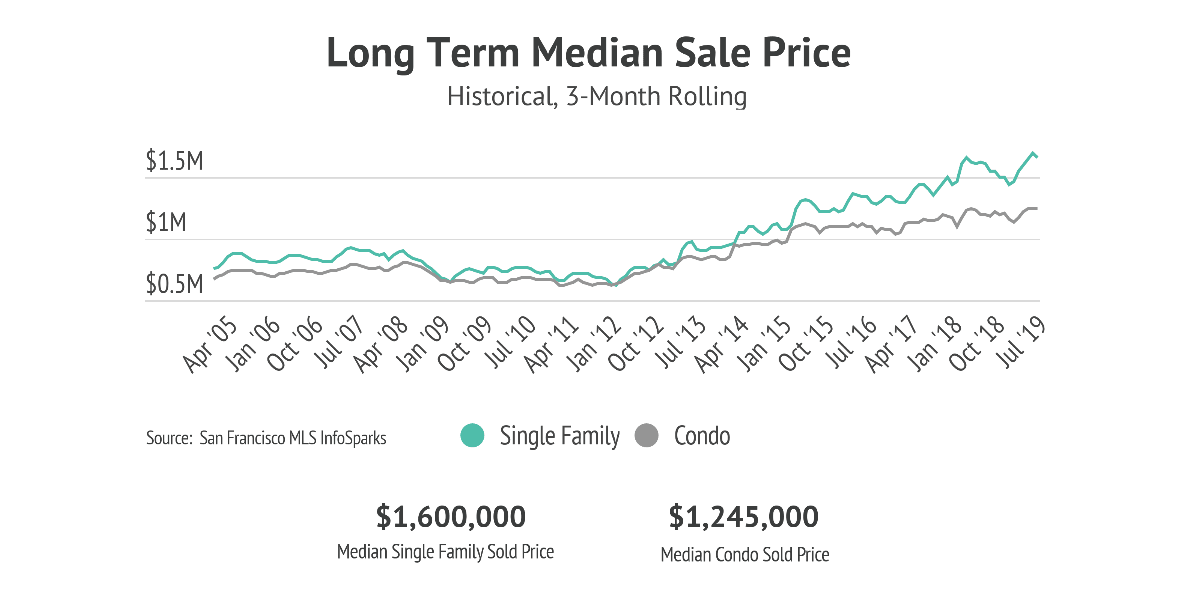

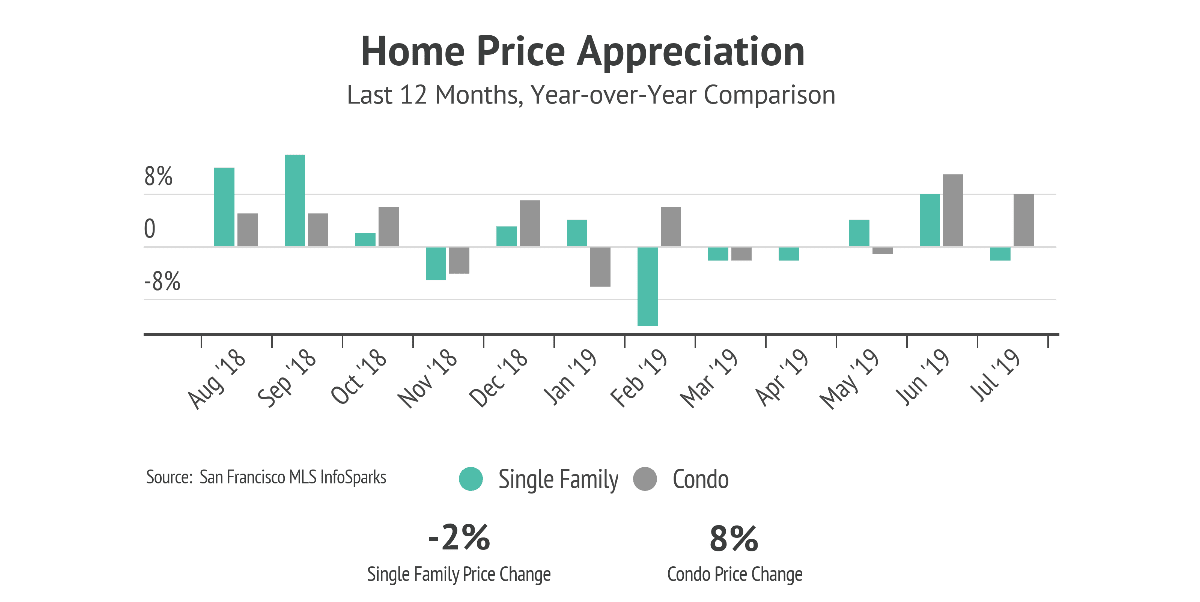

However, something curious happened in July. Despite rates maintaining record lows, San Francisco home prices are down by 7%, as compared to the previous month, and down 2% year-over-year. This is the first time prices have dropped on a yearly basis since April 2019.

Normally, there’s an inverse correlation between interest rates and home prices in that lower mortgage rates are usually a boon to the housing market. This month, however, mortgage rates had little impact on the market overall.

|